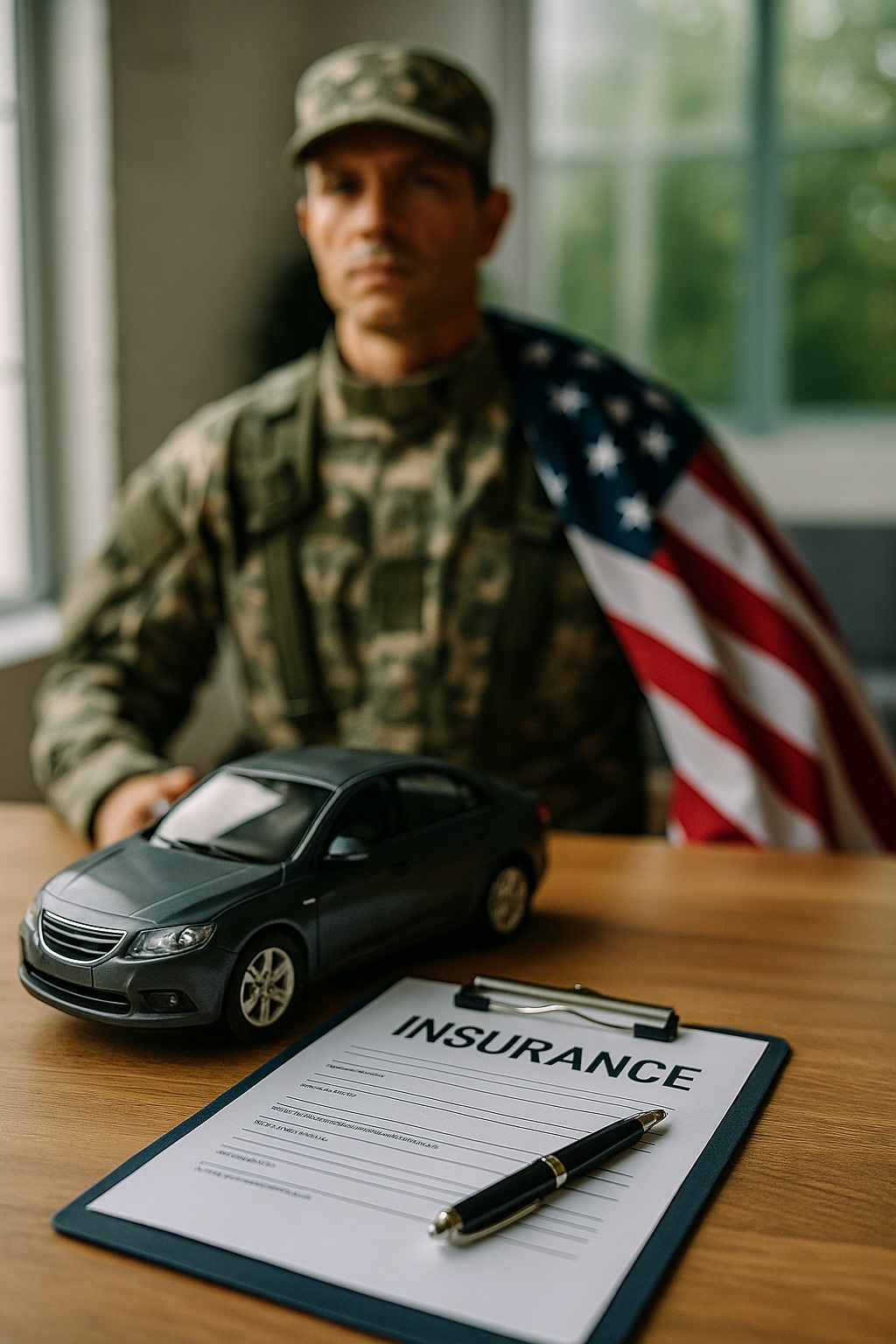

Military families face unique challenges and responsibilities, especially when it comes to financial planning. Insurance plays a crucial role in protecting those who serve and their loved ones. Understanding how to save on military insurance can make a significant difference in your budget and peace of mind. While many insurance providers offer special rates for military personnel, navigating the options can be overwhelming. However, with the right information, you can confidently secure the best coverage at the most affordable price. Learning about available discounts and strategies for maximizing these savings is essential. As you read on, you will discover practical tips and common pitfalls to avoid when seeking insurance savings tailored for the military community.

Understanding the Basics of Military Insurance Savings

Military insurance offers coverage specifically designed for service members and their families. Typically, it includes health, life, auto, and property insurance with unique benefits. Many providers recognize the risks and sacrifices associated with military life, so they offer policies with special features. For instance, some insurance plans provide flexible payment options for those deployed overseas. Additionally, eligibility for certain military insurance plans often extends to spouses and children, which helps protect the whole family.

Most military insurance providers offer discounted rates compared to civilian plans. These savings can come in the form of lower premiums, reduced deductibles, or bundled coverage options. Moreover, insurance companies may consider your service status when determining rates, sometimes leading to extra discounts. If you are active duty, reserves, or a veteran, check what benefits apply to your situation. Furthermore, some policies continue the savings even after you leave the military.

Understanding how these savings work is key to choosing the right policy. Take time to read the fine print so you know what is covered and what is not. Also, ask your provider to explain military-specific features, such as deployment cancellation or war zone exclusions. Sometimes, military insurance comes with built-in support for counseling or family assistance during tough times. Always compare several plans before deciding, as every provider structures savings differently. With careful research, you can find excellent coverage that respects your budget.

Key Benefits of Choosing Military Insurance Plans

Military insurance plans stand out because they are tailored to the unique needs of service families. Not only do they offer comprehensive coverage, but they also account for frequent moves, deployment, and changes in duty status. Furthermore, these plans often provide worldwide protection, a valuable feature for military members stationed overseas. For example, some policies ensure you remain covered in case of reassignment to a different country. You will also find many military insurers with flexible terms, making it easier to update or adjust your coverage as your needs shift.

Providers of military insurance usually offer excellent customer support that understands military life. Because agents are trained to address military-specific situations, you receive prompt and knowledgeable assistance. Additionally, many military insurance plans feature rapid claims processing, which becomes essential during emergencies or when stationed far from home. You can also access advice on protecting your family’s assets and planning for the future. This level of personalized support contributes greatly to peace of mind.

Many military insurance plans include perks beyond standard coverage. For instance, you might find extra benefits such as identity theft protection or discounted legal services. Some providers even offer exclusive access to member-only financial products or educational resources. These added features can further stretch your savings and provide value you may not find with civilian insurance. Altogether, choosing a military insurance plan means you get coverage designed for your lifestyle, often at a better price than standard plans.

How to Maximize Discounts on Military Insurance

To get the best savings on military insurance, start by gathering accurate information about your eligibility. Many providers offer different discount levels based on your service status, rank, or length of service. You should always ask about all available discounts, including those for safe driving, good grades for dependents, or multiple policy bundling. Not every discount is advertised, so do not hesitate to speak with an agent and request a full list. Staying informed ensures you never miss out on valuable offers.

Another effective way to maximize your discounts is by regularly reviewing and updating your policy. As your circumstances change, so do your insurance needs and eligibility for certain discounts. For example, if you move to a less risky area or install safety devices in your home or car, you could qualify for new savings. Many providers reward loyalty, so maintaining a long relationship with one company can unlock additional discounts over time. Always keep your profile updated to take advantage of every possible offer.

Comparison shopping is crucial when seeking the highest discounts. Take time to request quotes from multiple military insurance providers to identify the best options. Many companies compete for your business by offering unique incentives or price breaks. Utilize online comparison tools or work with a broker who understands military insurance plans. Not only will this approach highlight the biggest savings, but it can also help you find coverage that matches your specific needs. Remember, a little research goes a long way toward maximizing your insurance savings.

Common Mistakes to Avoid When Seeking Savings

One frequent mistake military families make is settling for the first insurance offer they receive. While it may seem convenient, failing to compare multiple quotes often means missing out on better deals. Insurance providers differ in the discounts and benefits they offer, so doing your homework is important. You can save more money by exploring all your options before committing to a plan. Never assume that all military insurance is the same, as coverage details can vary widely.

Another common error is not updating your insurance information after life changes. For example, moving to a new base, getting married, or having children can affect your eligibility for savings. If you forget to inform your insurer about these changes, you might lose out on important discounts. Always keep your policy details current to ensure you qualify for every available benefit. Timely updates also help avoid potential problems when filing a claim.

Some people mistakenly think cheaper coverage is always better. However, choosing the lowest-priced plan without considering your actual needs can leave you underinsured. While saving money is important, balance affordability with adequate coverage for your situation. Take time to carefully review what each policy includes and excludes before making a decision. Focusing only on price could cost you more in the long run if you lack protection when you need it most.

Long-Term Strategies for Growing Your Insurance Savings

Planning is one of the most effective ways to grow your military insurance savings over time. Start by assessing your current and future insurance needs so you can select policies that will remain suitable throughout your career. When you pick flexible plans that adjust with life changes, you avoid unnecessary costs and gaps in coverage. Regularly scheduled reviews help you stay aligned with your savings goals as your situation evolves.

Another powerful strategy involves taking advantage of bundled insurance products. Many providers allow you to combine auto, home, and life coverage for a reduced total premium. Not only does bundling save money, but it also simplifies managing your policies under one provider. Some companies offer loyalty rewards or additional discounts the longer you stay with them. Always inquire about long-term savings options when shopping for military insurance.

Lastly, focus on maintaining a good credit score and safe habits, as many insurers consider these factors when setting rates. Good financial standing can lead to better deals on premiums, especially for military families. Additionally, staying claim-free and practicing safety on the road and at home can further increase your savings. Participate in insurer-offered programs such as defensive driving courses or home security upgrades for added discounts. By making smart choices now, you set yourself up for even greater savings in the years ahead.

Conclusion

Saving on military insurance is not just about finding the lowest price, but also about securing the right protection for you and your family. With an understanding of the basics, you can confidently explore specialized savings options available to military members. Taking advantage of key benefits, such as flexible coverage and dedicated support, helps provide peace of mind during uncertain times. Remember to actively seek out discounts by regularly updating your information and comparing multiple providers. Avoid common mistakes, such as neglecting policy reviews or choosing inadequate coverage, so you do not lose out on valuable savings. Instead, focus on long-term strategies like bundling policies, maintaining good financial habits, and participating in insurer programs.